US indexes enter bear market as market prices in recession risks

Inflation has risen significantly due to supply disruptions arising from the Covid lockdowns, the Russian invasion of Ukraine, and China’s Covid-0 strategy. The recent US CPI release of 8.6% year on year to May was the highest since 1981 which prompted investors to price-in more aggressive monetary policy tightening (increasing interest rates) which has the flow-on effect of raising the risks of a recession. The World Bank recently slashed its global growth forecasts by nearly a third to 2.9% and released a firm warning that many countries were at risk of recession.

Against this backdrop, we analyse the impacts on Australian and US equities and the downside risk (risk of loss) potential of a recession. In our analysis we proxy the ASX200 with the Australian All Ordinaries (All Ords) index that contains the top 500 stocks in Australia, due to the All Ord’s longer price history. In our analysis we use the word drawdown to mean the peak to trough performance since 31/12/2021.

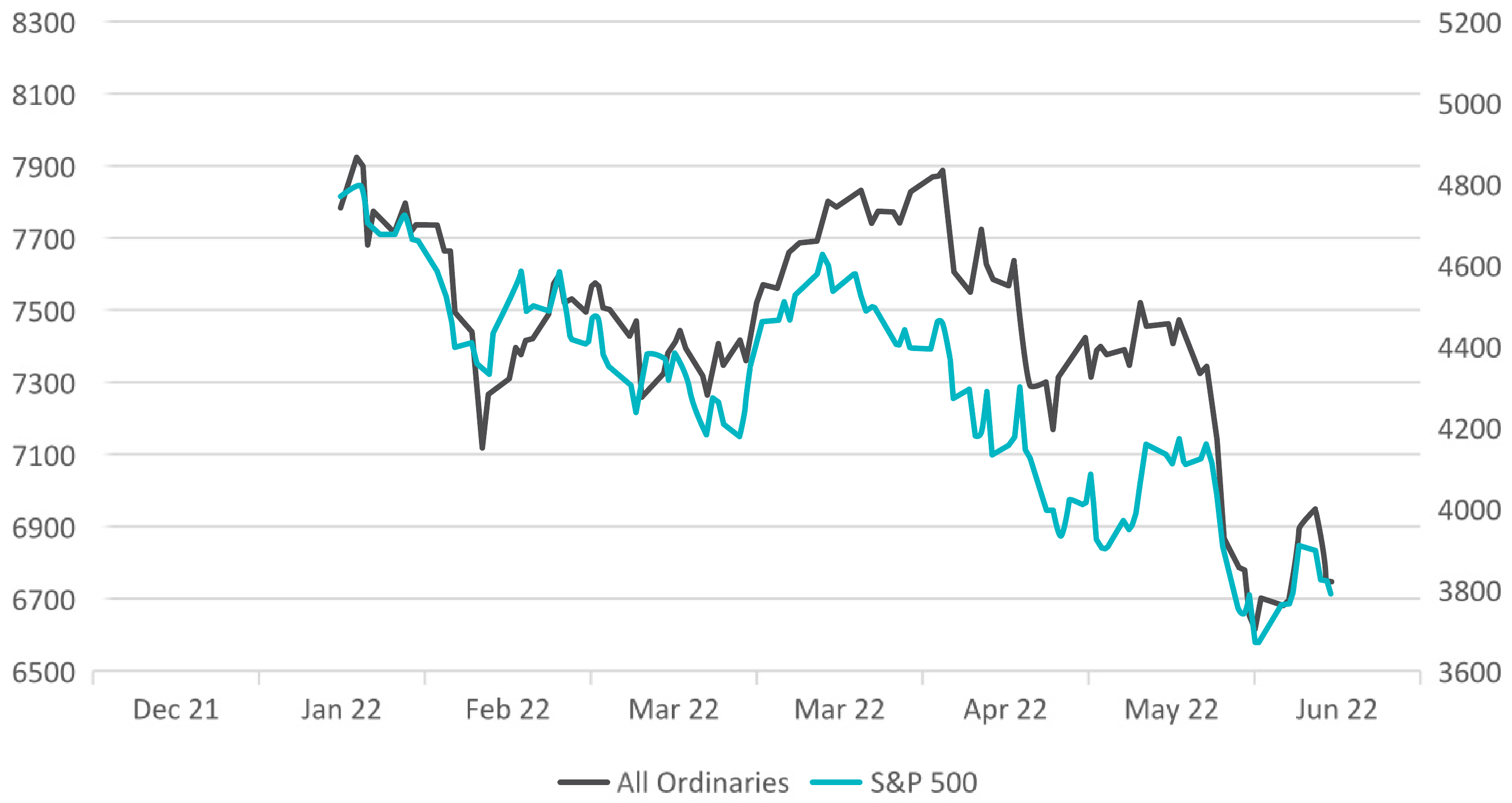

Graph 1: Comparison of S&P500 vs All Ordinaries CYTD Performance

*Source Bloomberg

Equities globally have fallen substantially from their early January peaks, particularly in the US, as the world grappled with persistent and historically high inflation. Australian equities have fared better benefitting from the high exposure (~30%) to the energy and materials sector that rose due to surging commodity prices following Russia’s invasion of Ukraine. In Graph 1, we see that the All Ords begun to outperform the S&P500 following the Ukraine conflict in late February, however, sold off aggressively by the end June as recession fears drove a broad sell off in risk assets that included commodities. In addition, Australia has a small exposure to the technology sector (~3.7%) which has borne the brunt of the equity weakness. By mid-June, the All Ords recorded a drawdown of 16.20%.

Table 1: Equity returns – Maximum drawdown and CYTD

| Asset Class | Index | Drawdown CYTD | *CYTD as at 30/6/2022 |

| Australian Equities | All Ordinaries | -16.20% | -13.28% |

| Global Equities | S&P500 | -22.42% | -20.58% |

| Global Equities | NASDAQ | -32.76% | -29.51% |

*CYTD (Calendar year to date) performance is the return between 31/12/2021 to 30/06/2022

Table 1 compares the drawdown and calendar year to date return of Australian and Global equities (S&P500 and Nasdaq). The NASDAQ index recorded the highest drawdown and was down -32.76% peak to trough. The S&P recorded a drawdown of -22.42%, and The All Ords was the best performing of the three, recording a drawdown of -16.20%. The NASDAQ and S&500 have also entered bear market territory, marked by a drop of 20% or more from recent highs. Aggressive rate hikes typically have a significant impact on growth and tech companies as they see the bulk of their future years’ revenue discounted back at a higher interest rate, leading to lower valuations.

Record Inflation increase recession risks

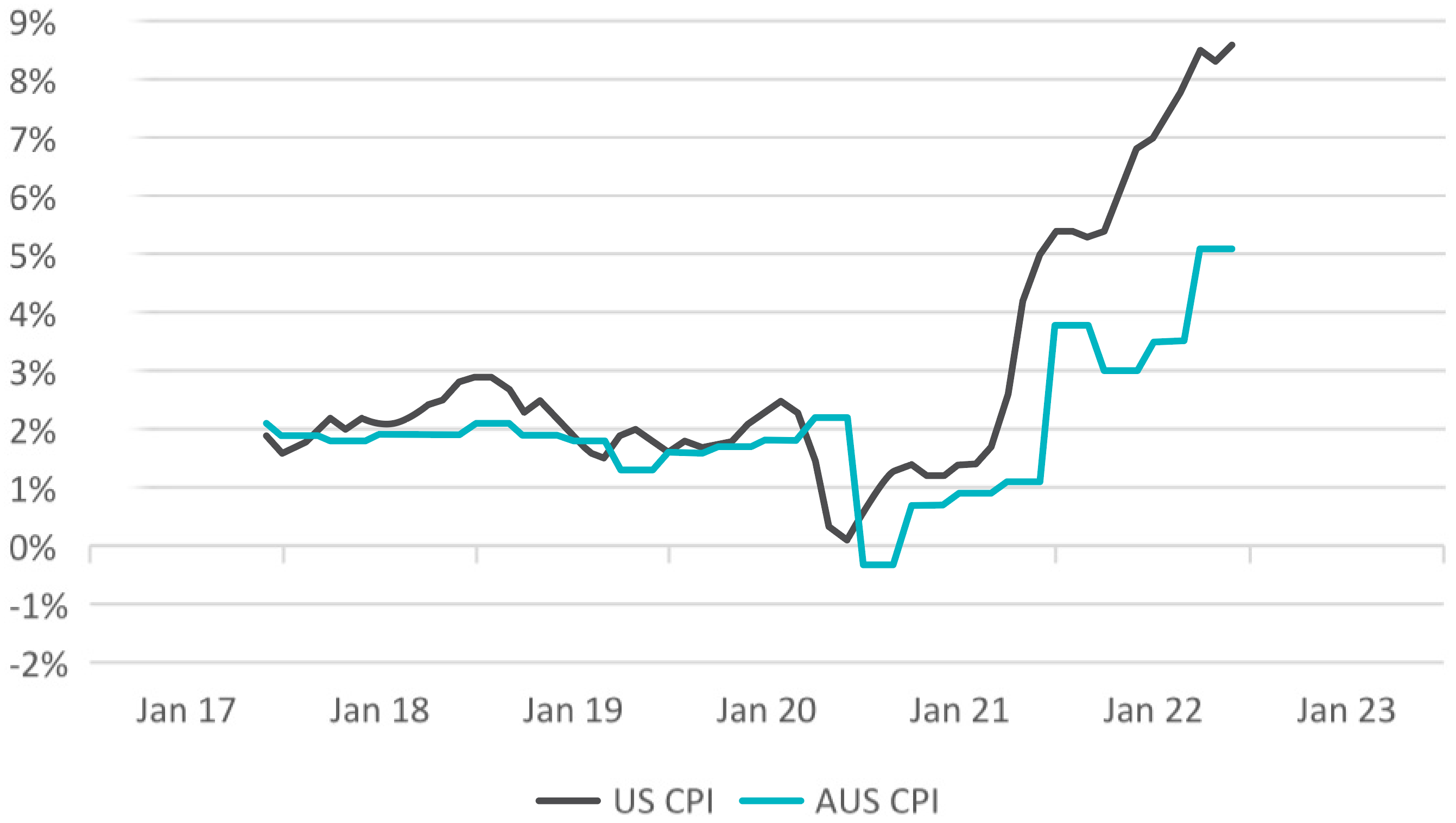

Graph 2: US vs Australian Inflation YoY

*Source Bloomberg

Graph 2 shows the US CPI rising to 8.6% in May 2022, the highest in 41 years, with Australia following behind on 5.1%, its highest in 20 years. Strong prices were seen across the board including energy, food, housing and travel. Contributing factors include the continuous supply chain issues caused by lockdowns, the Ukraine war and its impact on oil and agriculture exports and China’s Covid-0 strategy. Surging post-covid demand also contributed to inflation, aided by record fiscal and monetary stimulus.

To combat inflation, central banks globally unwound trillions in Covid stimulus, reducing the money supply and increasing the cash rate aggressively to deflate demand. By mid-June, the Fed tightened the policy rate by a cumulative 150bps with the latest rate hike of 75 bps, the single largest rate rise in 28 years. In contrast, the RBA recently hiked rates by 50bps in their June meeting, adding to the 25bps hike in May.

As central banks step up monetary responses to quell inflation, investors are increasingly concerned that large rate rises will introduce significant head winds to economic growth that could ultimately tip the economy into a recession.

Market Returns during a recession and in the subsequent years

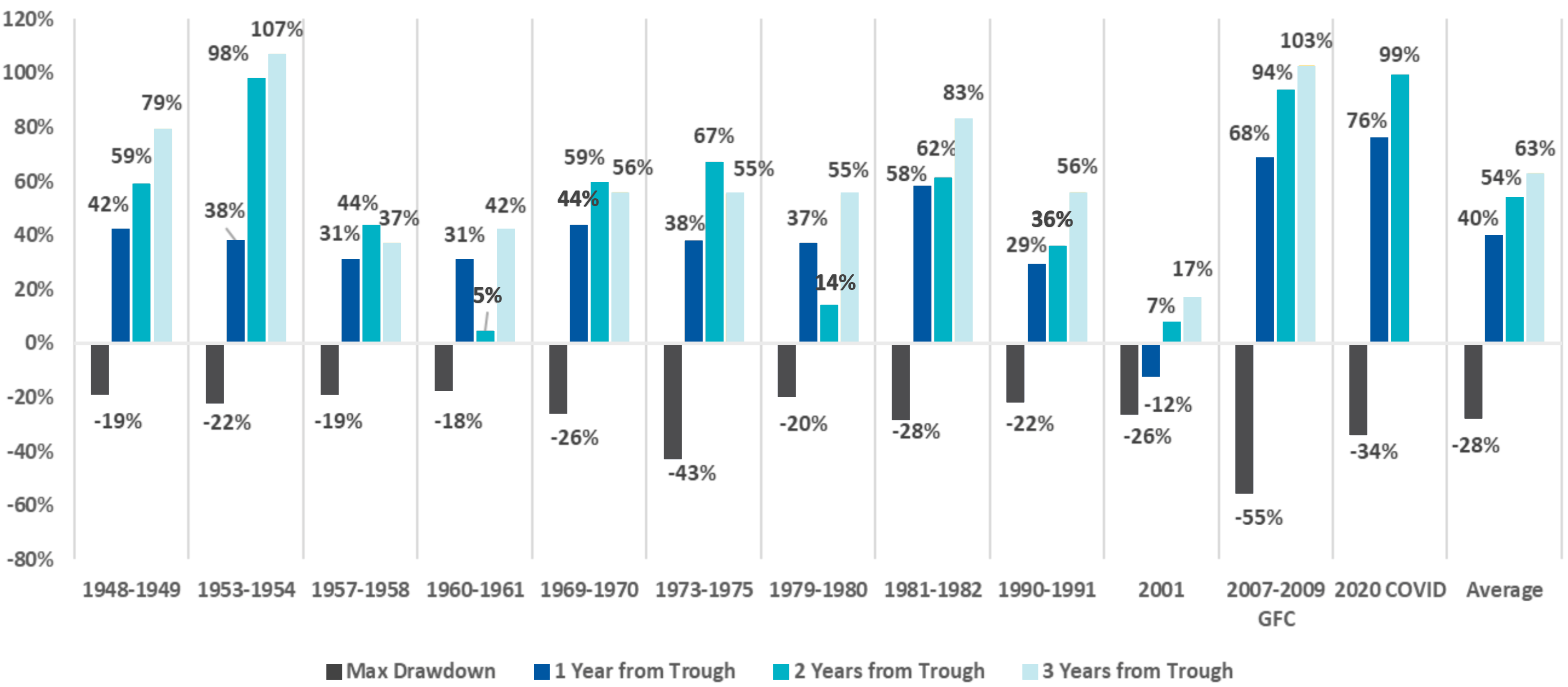

Graph 3 and Graph 4 below look at S&P500 and All Ords returns during each recession recorded since the end of World War 2. We also include the GFC drawdowns in the All Ords analysis as the index suffered a large drawdown in this period. Although there was no technical recession in Australian during that time, there was a sharp contraction in GDP growth along with an increase in the unemployment rate. A technical recession is marked by two consecutive quarters of negative growth in GDP.

Graph 3: S&P500 Recession Drawdown and 1-3 Year Post Drawdown Performance

*Source Bloomberg

In Graph 3 we see that the average drawdown of the S&P500 in a recession has been around 28%. The S&P500 currently has a drawdown of 22.42% from its peak and is effectively pricing in at least a 75% chance of recession. If history is anything to go by, it implies further downside risk which could see the index fall to 3453. The US recorded Q1 2022 GDP growth of -1.6%. It is the first contraction since the COVID19-induced recession in 2020 due to record trade deficits, supply constraints, worker shortages and high inflation. Q2 2022 US GDP growth data will be released in late July, which may see the US in a technical recession if it reveals a second quarter of negative growth.

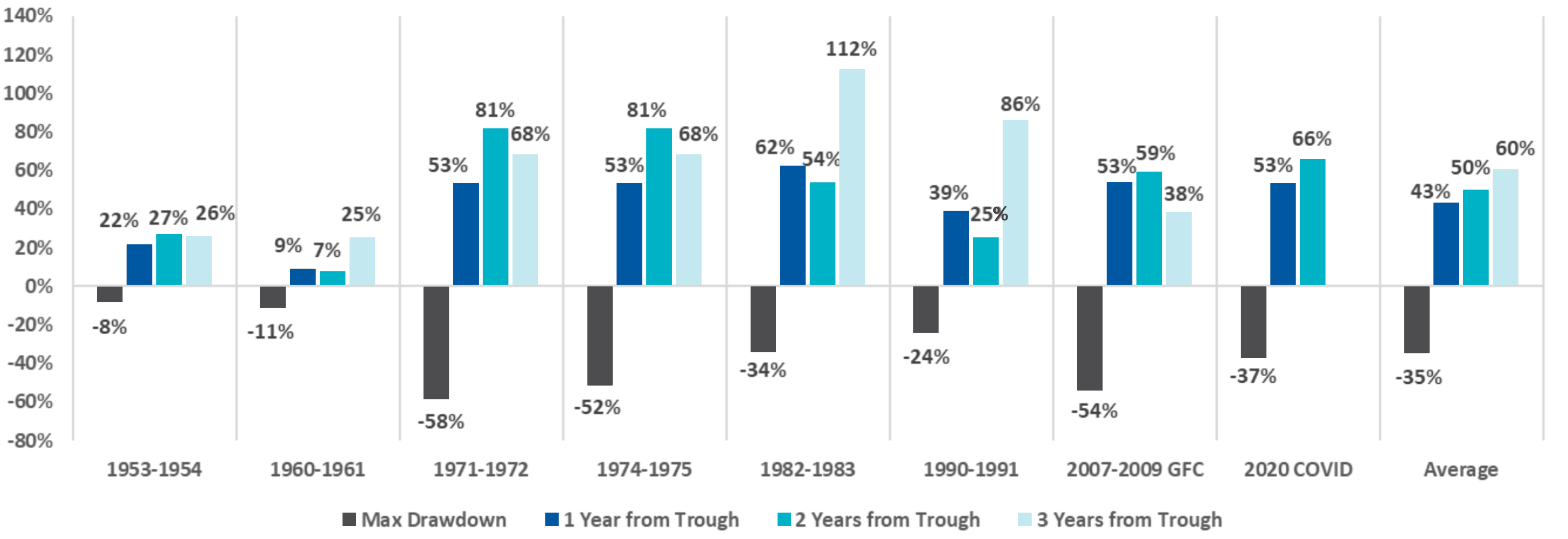

Graph 4: All Ords Recession Drawdown and 1-3 Year Post Drawdown Performance

*Source Bloomberg

In contrast, the average drawdown of the Australian All Ordinaries index across all recessions since the 1950’s was 35%. The All Ords currently has a drawdown of 16.20% and is effectively pricing in a 38% chance of recession. If Australia entered a recession, we could expect the All Ords to fall to 5152 based on historical performance. Australia’s Q1 2022 GDP growth rate was 0.8%, so there is a lower probability of a recession compared with the US, however, we note that growth is slowing as the previous Q4 2021 growth rate was 3.4%.

Most importantly, both graphs point to one common theme – don’t panic, and that it is important to remain invested (i.e not timing the market, but time in the market). The average returns 1 year after a recession drawdown is 40% for both US and Australian equities. After 2 years, this rises to 54% and 50% respectively. Holding for 3 years returned 63% and 60% respectively, with persevering investors recovering at least their recession drawdowns. Whilst the average case can be reassuring, caution is advised if the maximum drawdown is in excess to the average. This is a possibility given that China could face new coronavirus outbreaks, leading to more lockdowns and the war in Ukraine could stretch on and potentially draw more countries into the conflict. Both situations could very well exacerbate fragile supply lines and fuel inflation.

Action taken in CCIAM portfolios

CCIAM has undertaken several steps to manage risk within portfolios. In December 2021, risks were reduced by underweighting Australian and Global equities compared to the long-term strategic asset allocation (SAA). In addition, with the expectation of higher rates, the Fixed Income portfolios were also reduced with the weighted average duration shortened (lesser time to maturity) to preserve capital. Duration measures a fixed income portfolio's price sensitivity to interest rate changes. Overall, these actions resulted in the portfolios outperforming their SAA and highlighted the added value of dynamic asset allocation (DAA), particularly as a tool to mitigate risk and improve risk adjusted returns. The team also successfully participated in a number of buybacks, where client portfolios benefited froman additional average return of 20bps.